Fraud is the F word of business.

Fraud is legally defined by CAL. CIV. CODE § 3294 (3) as “an intentional misrepresentation, deceit, or concealment of a material fact known to the defendant with the intention on the part of the defendant of thereby depriving a person of property or legal rights or otherwise causing injury”.

In a business context, fraud basically is stealing or misappropriating the company’s assets in a devious manner, whether those assets are cash, inventory, intellectual property, business opportunities, or human resources.

Fraud is greatly underreported in the United States. Much of this is due to the victim company not being aware that fraud has been committed.

There are unlimited ways that fraud can be committed. Business owners should be alert as to how fraud can be committed within their organization as well as by outsiders against their organization. Examples of potential perpetrators inside and outside of the organization would be employees, vendors, customers, competitors, and others.

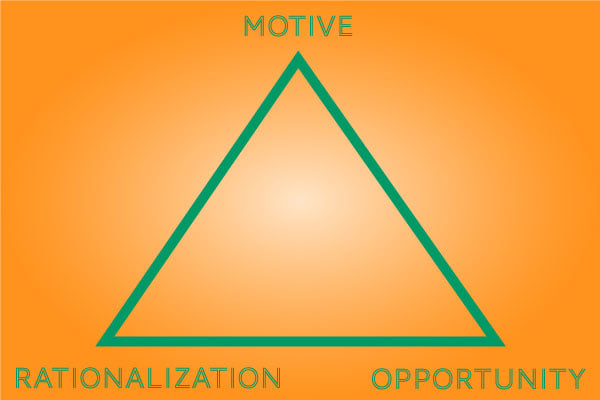

The Fraud Triangle

Studies have revealed that fraud will be attempted when the three elements of motive, rationalization, and opportunity exist in the mindset of the fraud perpetrator. Motive, rationalization, and opportunity are the elements of what is referred to as the Fraud Triangle. The Fraud Triangle is a visual depiction of when Fraud will occur. Fraud occurs when all three components are present:

Motive

Motive is a need that the fraudster has for some asset resource that the company has for personal use. Example of a motive or need would include having a drug or gambling addiction, a mistress, living beyond their means, desire to inflict damage, etc.

Rationalization

Rationalization is the reasoning that the fraudster uses to justify the act of fraud against the company. An example would be an employee who feels that he is underpaid, overworked, etc.

Opportunity

Opportunity for fraud to occur is usually the result of a flaw in the company’s internal control system, which provides the fraud perpetrator a chance to misappropriate (steal) the company’s assets. An example of this would be having no checks and balances in the accounting department, therefore it would be much easier to cover up the fraud by cooking the books.

When all three of those components exist simultaneously FRAUD will most likely occur.

An example of all elements of the Fraud Triangle existing simultaneously would be an employee needing money to support a drug habit (MOTIVE), he dislikes the business owner because he feels mistreated (RATIONALIZATION) and has access to the company’s inventory of copper piping, which can be sold for cash and is in charge of keeping the records for the inventory of copper piping (OPPORTUNITY). The employee will most likely commit fraud by stealing the copper piping and attempting to conceal the crime by altering the accounting records.

If one of the components in the fraud triangle is missing, fraud most likely will not occur.

The opportunity component of the Fraud Triangle is the element, which is most controllable by the business owner. The business owner can minimize the opportunity component by designing and implementing a good system of internal controls, which would include checks and balances (segregation of duties), as well as management oversight and review. Even if the fraud does occur, the crime will be revealed and detected in a more timely manner (which is a fraud deterring mechanism in and of itself). Internal control systems should be designed with cost and benefit considerations. A prefect internal control system does not exist and would be very costly. An overview of internal controls will be the subject of an upcoming article.

The rationalization component can be partially controlled by the business owner’s design of a good work environment, which does not engage in illegal employment practices and creates an environment which encourages employee engagement. Employee engagement will be the subject of an upcoming article.

The motive component of the Fraud Triangle is most difficult for the business owner to control since it relates to the state of mind of another person. Best practices in detecting motive would be to have an awareness of employees that recognizes red flags of behavior, which might indicate a need for resources beyond their compensation levels or some other motivation, which may lead to fraudulent activity.

Fraud from parties outside the organization.

Fraud can be committed against a company by its vendors, customers, competitors and professional criminals. The most effective way to mitigate this is to have a good system of internal controls, which is able to prevent and detect fraud. The specific control procedures that can reduce the risk of fraud from outside parties, is the subject of an upcoming article. Computer fraud is also rampant in our modern internet connected world. A recent study indicated that the production of “malware”, that is software designed to compromise and steal information from systems; greatly exceeds the production of legitimate commercial software. Best practices to ensure that your company is safeguarded from these threats, will be the subject of an upcoming article.

About the Authors

|

Amir Aghevli, CPA, CGMA, CA Real Estate Broker, is a partner of Milam, Knecht & Warner, LLP. He is in charge of attestation, accounting, auditing, and business consulting at MKW. |

|

Randy Taix, CPA, is a senior accountant at Milam, Knecht & Warner, LLP. He has been in public accounting for 7 years, with experience in both audit and tax engagements. |