A new method of providing pre-tax investment opportunities to key employees

Many business owners and companies utilize 401(k) plans or similar type plans for their employees. And they should. 401(k) plans have the most attractive features of any investment available in the marketplace, (i) pre-tax deferrals on compensation, and (ii) tax deferred compounding on those dollars.

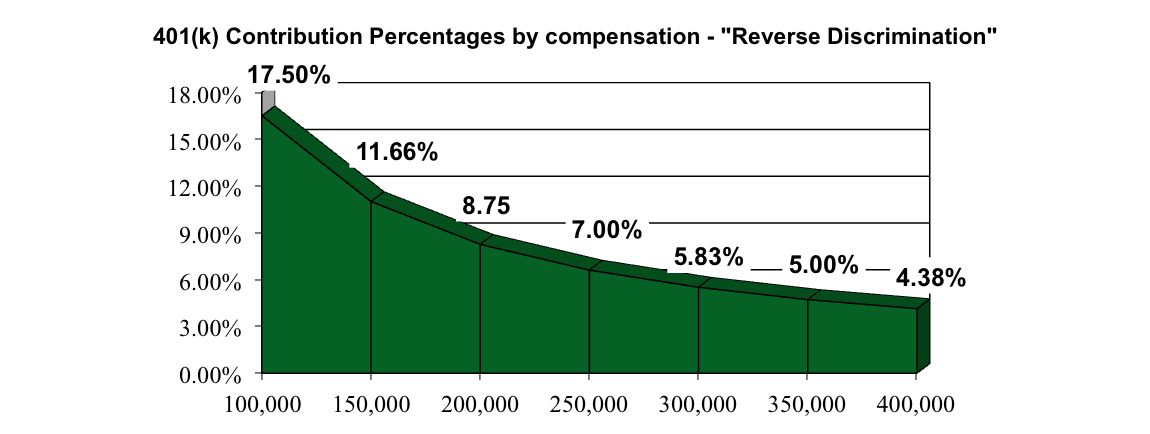

However, the problem for “highly compensated employees” (HCEs) is that it is just not enough. HCEs generally would like to defer more. 401(k) plans have caps and HCEs cannot put in the same contribution percentages as lower salaried employees. So, HCEs are stuck. HCEs want and should be able to contribute the same percentage of compensation into a 401(k) as broad based employees but they are limited under IRS guidelines. I like to call this dilemma, “reverse discrimination”. The chart below depicts the imbalance in this situation. The horizontal axis indicates the increase in compensation while the vertical axis shows the contribution percentage that can be made in a 401(k) plan.

_contribution_precentages_by_compensation_reverse_discrimination.png?width=800&height=301&name=401(k)_contribution_precentages_by_compensation_reverse_discrimination.png)

There is a common solution to this dilemma that has been available for years for larger companies. Over 80% of Fortune 500 companies have “nonqualified” deferred compensation plans that allow HCEs to defer additional pre-tax amounts above the company 401(k) plan[1].

The horse power associated with these plans is that participants can defer unlimited amounts on a pre-tax basis. There are no caps! Furthermore, it can only be designed for HCEs due to the nature of the plan. Broad based employees are prohibited from participating[2].

As attractive as these plans are for large corporations, small and mid-sized business owners have always been handcuffed from providing this type of plan due to the fact that any compensation deferred in a nonqualified plan remained on the books of the company. Compensation amounts contributed were not deductible. However, there is now an answer for small to mid-sized companies to get involved with nonqualified deferral plans.

A Pre-Tax Deferral Solution

Until recently, the only additional benefit alternatives for small and mid-sized companies involved either offering a different type of qualified plan (e.g. Defined Benefit) or perhaps “safe harboring” the existing 401(k) plan. There is a more straightforward, compliant, and cost-effective solution that I refer to as the 409A PLUS Supplemental Retirement Program. 409A PLUS is designed so that owners and executives can elect to defer up to 100% of their taxable income on a tax advantaged basis through plan contributions and in full compliance with IRC Section 409A[3].

Through an alliance with two national lending partners, 409A PLUS enables your business to leverage the plan assets, which remain on the company’s balance sheet, to support business cash flow, maximize plan contributions, and off-set taxes that are temporarily shifted from employee participants to business owners. The lending partners have tailored financing programs specifically designed to address the program’s requirements, be easily underwritten, and without the requirement for business owner personal guarantees. Additionally, the 409A PLUS program is designed to provide the funds to pay off the loan balance while simultaneously delivering long-term growth potential to fund retirement needs. No additional collateral is necessary to be established outside of the plan to secure the loan.

409A PLUS enables business owners and HCEs to accumulate retirement funds without the drag of temporary tax costs. The value is that HCEs now have the advantage of keeping approximately 90% of their nonqualified retirement savings dollars working for them during accumulation, versus 50-60% after-tax dollars. By having more retirement assets growing on a compound basis, plan participants aren’t compelled to ‘chase’ returns or incur unnecessary risks. Meeting retirement goals using appropriately conservative, reliable return objectives is now realistic.

Owners and HCEs of “pass through” business entities may now take advantage of leveraging nonqualified deferred compensation plans whereas before, there was minimal, if any benefit to this retirement strategy. 409A PLUS provides this alternative by simply eliminating the traditional negative cash flow impact.

Hypothetical investor age 45 making a $100,000 contribution each year for 14 years; 7% crediting rate net of investment management fees; benefits paid over 20 years.

Hypothetical investor age 45 making a $100,000 contribution each year for 14 years; 7% crediting rate net of investment management fees; benefits paid over 20 years.

If you would like more information on the 409A PLUS Supplemental Retirement Program, please feel free to email me or call me at (213) 412-2808.

|

Monte Harrick is a managing director of VerityPoint, a national benefits consulting firm headquartered in Los Angeles. He has extensive experience in working with businesses in designing, financing, securing, and administering nonqualified and supplemental benefit plans. |

[1] Marsh Executive Benefits; Nonqualified Deferred Compensation marketing flyer, January, 2011

[2] The reason for this is the “risk of forfeiture” associated with these benefits. The IRS indicates that to have all the generous provisions that are contained in deferred compensation plans, (pre-tax deferrals, tax deferred compounding, etc.) there needs to be some risk to participants. This risk is bankruptcy and the potential forfeiting of a participant’s account balance. Plans can be designed to protect benefits in a change in control but that is for another discussion.

[3] IRC 409A is the Internal Revenue Code governing nonqualified deferral plans.